VA Loan Closing Costs: What to Expect and How to Save

When I began researching VA loans, the first thing that kept coming up was closing costs. This was an extra complexity I didn’t really need. What, in fact, is that va loan closing costs, who pays them, and how bad are we talking? I assumed it was finally time to crack this all open, so I have a better idea of what the process might look like when I close on my home. Well, it turns out that getting a sense of these expenses is crucial for budgeting.

Who Pays VA Loan Closing Costs?

With a VA loan, both the buyer and seller can pay closing costs depending on the loan agreement and negotiations. VA buyers commonly pay lender fees, appraisal charges, prepaid taxes, homeowners insurance, and the VA funding fee.

Sellers are also allowed to cover many closing expenses and may contribute up to 4% of the loan amount in seller concessions, helping veterans reduce upfront costs.

In most cases, VA loan closing costs range from 2% to 5% of the home’s purchase price. The Department of Veterans Affairs also limits certain fees to protect military borrowers from excessive charges.

What Are VA Loan Closing Costs?

As I began researching purchasing my first home with a VA loan several years ago, the term “closing costs” seemed to be everywhere. To be brutally honest, it sounded like a fancy excuse for them to take my money before I even had the keys in hand.

But after investigating further, not as terrifying as it seems. Essentially, closing costs are simply the fees and expenses you will need to pay in order to secure your mortgage and finally take legal ownership of a property.

Think of it like the last few paperwork and service fees which assist in making the deal happen. Note: these expenses are in addition to your down payment and most likely had to be paid at the same time as you closed on when buying a house.

This includes a whole host of things, from lender fees through to government charges. It is best to try and wrap your mind around these so you’re not caught off guard when the time comes. These costs typically range from 2% to 5% of the loan amount, but will vary. This is a big part so you have to plan ahead.

So here is brief overview of standard closing cost.

- Lender fees: these are the costs from your mortgage company for processing, underwriting, and approving your loan. The VA actually limits the amount of those, such as the origination fee, limiting it to typically 1% or less.

- Third-Party Services: These are things like appraisals to verify the home value, title searches that ensure ownership by examining recorded documents and possibly many more. However, one of these services include insurance for your property in case someone comes along later claiming they own part or all of it (title insurance).

- Prepaids: You may have to pay some of these items upfront for a set period, including homeowners insurance and property taxes. This way their bills are taken care of right off the bat.

- Governmental Fees: These are fees to record the deed and mortgage at local government offices.

Keep in mind that while VA loans have a unique loan structure, closing costs are part of every mortgage type, and lenders must follow the rules about who (the borrower or lender) pays which fees.

It is a huge benefit of using your VA loan because it helps you to keep the cost out-of-pocket lower than other loans. The VA tries to shield service members and veterans from high fees.

Being aware of these expenses is a great start to the process of buying your new home. This is due not only to the amount of the loan, but also to all costs associated with it. Knowing these origination and funding fees will enable you to budget accurately

Common VA Loan Closing Costs

When I was going through the VA loan process, I quickly realized there’s a whole list of VA home loan settlement costs that come with buying a house. It’s not just the price of the home itself; there are a bunch of fees and charges that pop up right at the end.

Understanding what are VA loan closing costs is pretty important so you don’t get surprised. These VA home loan closing expenses can add up, and knowing them beforehand helps a lot with budgeting.

Title Insurance and Escrow Fees in VA Loan Closing Costs

These are pretty standard for most home purchases, not just VA loans. Title insurance protects both me and the lender against any ownership claims or title defects that might show up later.

The title search itself makes sure the seller actually has the right to sell the property to me. Escrow fees cover the cost of the neutral third party that handles all the paperwork and funds during the closing process. It’s like a middleman making sure everything is done correctly.

Appraisal and Inspection Fees for VA Loans

So, the VA requires an appraisal to make sure the home is worth what I’m borrowing. This fee pays for the appraiser to check out the property. Sometimes, depending on the area, there might be other required inspections, like for termites or well and septic systems if the house has them. I had to pay for these upfront, which felt like a chunk of money right away.

Lender Origination Fees

This is basically the fee the lender charges for processing, underwriting, and approving my loan. The VA puts a cap on this, limiting it to 1% of the loan amount. It covers their work in getting the loan set up for me. It’s one of those standard VA home loan closing expenses that’s pretty much unavoidable.

Prepaid Costs

These are costs that are due at closing but cover expenses that will come up later in the year. Think of things like homeowners insurance premiums and property taxes.

My lender usually requires me to pay a portion of these upfront to set up an escrow account. This way, they know those bills will be covered. It’s a bit of an upfront hit, but it spreads out those big annual or semi-annual bills.

It’s good to remember that while many closing costs for VA mortgages are regulated, some can vary by lender and location. Always ask for a detailed breakdown of what are closing costs for VA loans so you know exactly what you’re paying for.

It’s also worth noting that some of these VA loan closing costs can be rolled into the loan itself, which is something I looked into.

This means you can finance some of these expenses, though it does increase your overall loan amount and the interest you’ll pay over time. It’s a trade-off to consider when figuring out how to manage paying closing costs on VA loan.

Can VA Loan Closing Costs Be Negotiated?

When I was going through the VA loan process, I wondered if I could actually haggle on any of those closing costs. It felt like a big chunk of money, and I wanted to see if there was any wiggle room. The good news is, yes, you absolutely can negotiate some aspects of your VA loan closing costs. It’s not like everything is set in stone.

One of the biggest areas for negotiation is with the seller. Sellers can actually pay for a portion of your closing costs, which is a pretty sweet deal. They can contribute up to 4% of the purchase price towards your closing costs.

This can cover a lot of different fees, like appraisal fees, title insurance, and even some of those prepaid items like taxes and insurance. It’s definitely worth bringing up during your offer negotiation. You might also be able to get the seller to pay your VA funding fee, which can be a significant amount.

Then there’s the lender. While they might not be as open to negotiation as a seller, I found that some lenders are willing to offer credits. These are called lender credits. Basically, in exchange for a slightly higher interest rate on your loan, the lender will give you a credit at closing to help cover some of those costs.

It’s a trade-off – a little more interest over time for less cash out of your pocket right now. I always suggest comparing offers from a few different lenders because their willingness to offer credits can vary a lot. Shopping around for your lender is a smart move. Comparing offers from different lenders can help you find the most competitive rates and fees.

Here are a few things to keep in mind when you’re thinking about negotiation:

- Review your Loan Estimate carefully: This document breaks down all the estimated costs. Look at each line item and see if there’s anything that seems unusually high or if there’s room for adjustment.

- Understand what’s negotiable: Some fees are pretty standard and set by third parties (like appraisal fees), but others, like origination fees or lender credits, can be more flexible.

- Don’t be afraid to ask: The worst they can say is no. It’s your benefit, and you should feel comfortable asking questions and exploring all your options.

It’s important to remember that while negotiation is possible, there are still VA-mandated limits on certain fees. The VA itself has rules about what costs are allowed and what can be charged, so not every single fee is up for grabs. Always check with your loan officer about what’s permissible under VA guidelines.

Ultimately, being proactive and informed about your closing costs can make a big difference in how much cash you need to bring to the closing table. It’s all about understanding the different players involved and what you can realistically ask for. Negotiating VA closing costs can lead to significant savings, so it’s worth the effort.

Average VA Loan Closing Costs

So, how much are VA loan closing costs, really? It’s a question I get asked a lot, and honestly, there isn’t one simple number. Think of it like this: VA loan closing fees can really add up, and they tend to fall somewhere between 3% and 5% of your total loan amount.

For example, if you’re looking at a $300,000 loan, you might be staring down anywhere from $9,000 to $15,000 in these fees. It really depends on the lender you pick and where you’re buying.

Here’s a quick breakdown of what you might see:

- Origination Fees: Lenders can charge up to 1% of the loan amount for processing your loan. Sometimes they charge a flat 1%, other times they itemize it, but it shouldn’t go over that 1% mark.

- Appraisal Fees: The VA requires an appraisal to check the home’s value and condition. These typically run from $650 to $1,300.

- Title Insurance and Escrow: This covers things like searching property records and insuring the title. Costs can vary quite a bit.

- Prepaid Items: You’ll likely need to prepay some property taxes and homeowners insurance premiums.

It’s important to remember that the VA actually limits what closing costs buyers can pay. This is a big perk of the VA loan, helping to keep your out-of-pocket expenses lower compared to other loan types. Sellers can also contribute, covering up to 4% of the sales price in concessions, which can really help offset these costs.

When you apply for a VA loan, your lender is legally required to give you an estimate of these costs within three days. Then, right before you close, you’ll get a final breakdown. This transparency is key, so you know exactly how much are VA loan closing costs for your specific situation.

Don’t forget to factor in the VA funding fee, which is a one-time charge that can sometimes be rolled into the loan itself, though that will increase your monthly payments [f108]. Overall, while there’s no single average VA loan closing fee, understanding these components helps you prepare for the total amount you’ll need to have ready.

How to Estimate Your VA Loan Closing Costs

Restrictions, but it’s definitely doable. The first real step I took was to request a Loan Estimate from my lender. This is a critical document as it lays out all the projected costs you will incur. It’s not gospel, but it provides a pretty good ballpark figure.

Your lender must provide this estimate within three business days of you applying for a full loan. Be ready with income, credit info of course and the actual property you are looking at. Because of this the Loan Estimate will show you things like:

- Lender origination fees

- Appraisal fees: To determine the value and condition of the home.

- Title search and insurance costs.

- Property taxes and homeowners insurance are prepaid items.

- Discount points that you pay to reduce/ lower your interest rate

Remember, these are estimates. Retail, retail is almost always negotiable and some cost(s) may be pushed a bit around by the time real estate closes but there are only limited amount of fees that can increase. We can also confirm that VA loan closing costs typically range between 2%-5% of your mortgage amount.

So for a $300,000 loan you’re probably looking at $6k – 15k in total closing costs. Depending on your lender, loan amount and where the property is located, this range can change for either part of a house.

“Getting preapproved early and discussing a specific property with your lender as soon as possible is extremely important. The earlier your lender receives the property details, the more accurate your Loan Estimate will be, helping you make stronger offers and negotiate closing costs and loan terms with greater confidence.”

A comparison of the APR (As opposed to just the interest rate) proved useful also, in addition to obviously measuring values against what was shown on my Loan Estimate. So, the APR takes a lot of those closing costs into account so you can see what your total cost will be over time.

But you can also use an online calculator; just be sure to compare that with your loan estimate. Also, do not forget the VA Funding Fee, which is a one-time fee paid to the VA (but can sometimes be rolled in or paid by the seller). Knowing the parts of this process gives me a sense of control over the whole experience.

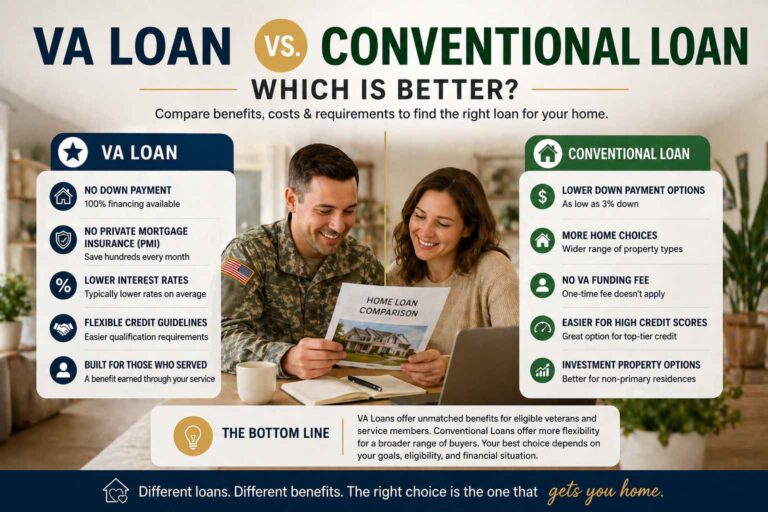

VA Loan Closing Costs vs Conventional Loan Costs

Before I started the mortgage process, a bunch of different loan types. I mean, it was kinda like a maze. What really struck me and was one of the big takeaways is how VA loan closing costs compared to a conventional. The good news is that the VA has certain safeguards in place to yank down your upfront cost.

First and foremost, the VA limits certain fees that conventional loans might not. The VA loan origination fee, which compensates the lender for processing and approving your home loan, is capped at 1% of the home’s purchase price.

This is actually a pretty nifty feature because conventional loans do not have that specific limitation, which would mean origination fees could potentially be higher. Being aware of these distinctions is useful when you are attempting to get a handleon your all out spending. A quick online search will turn up a VA loan closing cost calculator to give you an estimate.

Here’s a snapshot of some important distinctions:

Forbiden Fees: In fact, the VA itself prohibits borrowers from paying certain types of fees that are normally a staple with regular loans. VA borrowers can not have things like attorney fees and prepayment penalties. That means the lender or seller has to pay those costs.

Origination Fee Cap: As I just covered, the VA sets an upper limit of 1% for origination fees on a loan. This is a big protection that you don’t get with typical mortgages. This cap is typically highlighted when looking at a VA mortgage lender fees explained.

No PIW: This is a huge difference No Mortgage Insurance. If your down payment is less than 20%, conventional loans usually call for private mortgage insurance (PMI). FHA loans require their own type of mortgage insurance. Finally, VA loans do not require any mortgage insurance at all; you can save tens of thousands over the life of your loan and this lowers your closing costs too.

Seller Concessions: Sellers can pay towards closing costs on both loan types; however, the VA limits seller concesssions to 4% of the sales price. In some cases, conventional loans may allow even greater seller concessions.

“Understanding the VA loan closing cost breakdown is important. While both loan types include closing costs, VA loans often have fewer buyer-paid fees and certain charges are capped, making them a more affordable option for eligible veterans and active-duty service members.”

Always make comparisons between loan offers with the Loan Estimator your lender give you. This release will specify each of the individual costs.

Combine that with a VA loan closing cost calculator to find out the real total amount of money you are pulling from your pocket for transparent picture. Keep in mind that VA loan closing costs are usually between 3% and 5%, though these protections can help lower it more than you might expect compared to other types of loans.

Tips for Reducing VA Loan Closing Costs

So, you’re looking into how to reduce VA loan closing expenses? It’s a smart move. Nobody wants to pay more than they have to, especially when buying a home. Luckily, there are a few ways I’ve found to potentially lower those upfront costs.

First off, don’t underestimate the power of negotiation. While some fees are set, others might have a little wiggle room. Always ask your lender about any fees that seem high or if there are alternative providers they recommend for services like title insurance or appraisals. Sometimes, just asking can lead to a better deal.

Another big one is looking into lender credits. This is where the lender might cover some of your closing costs in exchange for a slightly higher interest rate on the loan. It’s a trade-off, for sure.

Your monthly payment will be a bit higher, but if you plan to move or refinance in a few years, it could save you a good chunk of cash upfront. It’s worth discussing with your loan officer to see if this strategy makes sense for your situation. You can even combine these with seller concessions, which are contributions the seller makes towards your closing costs.

Remember that VA loans have specific rules about what fees can be charged and who can pay them. Understanding these rules is key to making sure you’re not overpaying and that everything is structured correctly. Don’t hesitate to ask your lender to explain every line item on your Loan Estimate.

Here are a few more things to consider:

- Shop Around: Don’t just go with the first lender you talk to. Different lenders have different fee structures. Comparing Loan Estimates from a few different places can reveal significant savings.

- Seller Concessions: You can ask the seller to pay for some of your closing costs. There are limits to how much they can contribute, but it’s definitely something to explore during negotiations.

- VA Streamline Refinance: If you already have a VA loan and are looking to lower your interest rate, a VA Streamline Refinance, also known as a VA IRRRL, often comes with lower closing costs than a traditional refinance. Many of these costs can even be rolled into the new loan amount.

- Review Your Loan Estimate Carefully: Make sure you understand every fee listed. If something looks off or you have questions, ask for clarification immediately. This document is your best tool for seeing exactly what you’ll owe.

By being proactive and informed, I’ve found that managing and reducing VA loan closing costs is definitely achievable. It just takes a little effort and asking the right questions.

Common Mistakes with VA Loan Closing Costs (Avoid These Costly Errors)

As I went through the process of utilizing a VA loan, I came to find that there were some pitfalls when it comes to closing costs. With so much going on, you can get overwhelmed and okay some rules are pretty complicating. However, if you steer clear of these mistakes, it can earn you quite a bit smaller amount.

A major one, is not knowing actually the price you will be able to pay. There are some fees veterans can and cannot pay under VA rules. Examples include attorney fees or broker commissions for real estate that are generally not allowed to be charged to the buyer.

It’s a red flag if your lender attempts to charge these on top. Lesson 4: Insist on complete disclosure of all fees and check against VA limits Typically your lender or the VA will provide a list of such allowable and non-allowable fees. This is a good time to take the time and carefully review your Loan Estimate for anything unexpected.

Another common mistake is thinking that all closing costs are fixed. Some fees are pretty standard, while others — like lender origination fees — can be negotiated or offset at times. Origination fees are capped at 1% of the loan, but lenders may be flexible or you might look for lender credit.

These credits are often used to offset your closing costs but would add a marginal amount of interest, which may be worth it if you plan on staying in the home long term or refinancing later. It all boils down to understanding what your choice is.

Here are a few more things to watch out for:

Not budgeting for prepaid items: Closing costs are not just the fees themselves. You will also have to pay things like property taxes and homeowners’ insurance premiums for the next few months. These can add up quickly and should be included in your total cash needed at closing.

Not asking for seller concessions: A lot of the time, sellers can help you pay some money towards closing costs. Especially in a seller’s market, don’t be afraid to negotiate this. This will allow you to make sure your out-of-pocket expenses is very minimal

Not comparing lenders: Different lenders charge different fees. You can save thousands in your closing costs when you shop around by comparing Loan Estimates from several lenders. That is what limits many expenses the most efficiently.

“It’s important to stay proactive during the VA loan process. Don’t simply accept every number presented without understanding it. Ask your lender or loan officer to explain each fee clearly, and research anything that seems unclear. The VA loan program offers incredible benefits, but informed borrowers are in the best position to maximize those advantages.”

And last but not least, don’t forget the VA funding fee. It’s not a closing cost in the same way as, say, an appraisal fee is, but it’s paid up front and can be rolled into your loan balance.

Rolling it in, however, means you’ll be paying interest on that over the term of the loan, raising your monthly payments. Evaluate if you should pay it up front or finance this. Knowing all of these little nuances can really change your entire home-buying experience.

Wrapping It Up

So, that’s the lowdown on VA loan closing costs. It can seem like a lot at first, and honestly, I was a bit overwhelmed trying to figure it all out. But once I broke it down, it made more sense. Knowing what you can and can’t be charged for, and understanding that the seller can help out, really changes things.

It’s definitely worth taking the time to look over your Loan Estimate carefully and talk to your lender. Don’t be afraid to ask questions – that’s what they’re there for. Getting a handle on these costs upfront means fewer surprises later on, and that’s a good thing for anyone buying a home.

Frequently Asked Questions

What exactly are VA loan closing costs?

Think of VA loan closing costs as the final fees you pay to finalize your home purchase using a VA loan. It’s like a collection of small payments that cover all the paperwork, services, and checks needed to officially transfer ownership of the house to you and set up your loan. These costs are separate from your down payment and can add up, but the VA has rules to help keep them manageable for veterans.

Who usually pays for these closing costs?

It’s a bit of a mix! While I, as the buyer, will pay for some specific costs that are allowed, the seller can often cover many others. The VA has rules about who pays what to make sure veterans aren’t burdened with excessive fees. Sometimes, the lender might also offer credits to help reduce what I have to pay out of pocket.

Can I roll my closing costs into the VA loan itself?

Generally, I have to pay most closing costs upfront when I finalize the loan. However, there’s an exception: the VA funding fee, which is a one-time fee charged by the VA, can sometimes be included in the loan amount. Just remember, if I finance it, I’ll end up paying interest on that fee over time, making my monthly payments a little higher.

How much should I expect to spend on closing costs for a VA loan?

The amount can really vary, but typically, I’d budget for closing costs to be somewhere between 2% and 6% of the total loan amount. For instance, if my loan is $300,000, I might be looking at anywhere from $6,000 to $18,000 in closing costs. The exact figure depends on things like the lender I choose, where the house is located, and the specific fees involved.

Are there any closing costs that the VA won’t let me pay?

Yes, absolutely! The VA is protective of its borrowers and prohibits veterans from paying certain fees. These are often called ‘non-allowable’ fees. Things like real estate agent commissions and some attorney fees are typically not allowed for me to pay. If a fee falls into this category, either the seller or the lender usually has to cover it.

How can I get a good idea of my total closing costs before I commit?

Your lender is required by law to give you a document called a ‘Loan Estimate’ within three days of you applying for the loan. This paper will break down all the estimated closing costs. Later, closer to the closing date, you’ll get a final version. It’s super important to review these documents carefully to understand exactly what you’ll owe.