VA Loan vs Conventional Loan: Which Is Better?

Making that choice between a VA loan and conventional loan feels like such a monumental decision, mostly because as you’re attempting to navigate the best route for you in purchasing a home. I know I’ve been there.

They each have advantages and disadvantages, and knowing how it all compares against the other is fairly essential knowledge. VA loans provide some great benefits, such as no down payment for those who have served.

Nonetheless, traditional loans are best for many people, especially if you have savings for a down payment. Let’s look at how the VA loan vs conventional loan debate plays out and discover which is going to be a better solution.

Key Takeaways

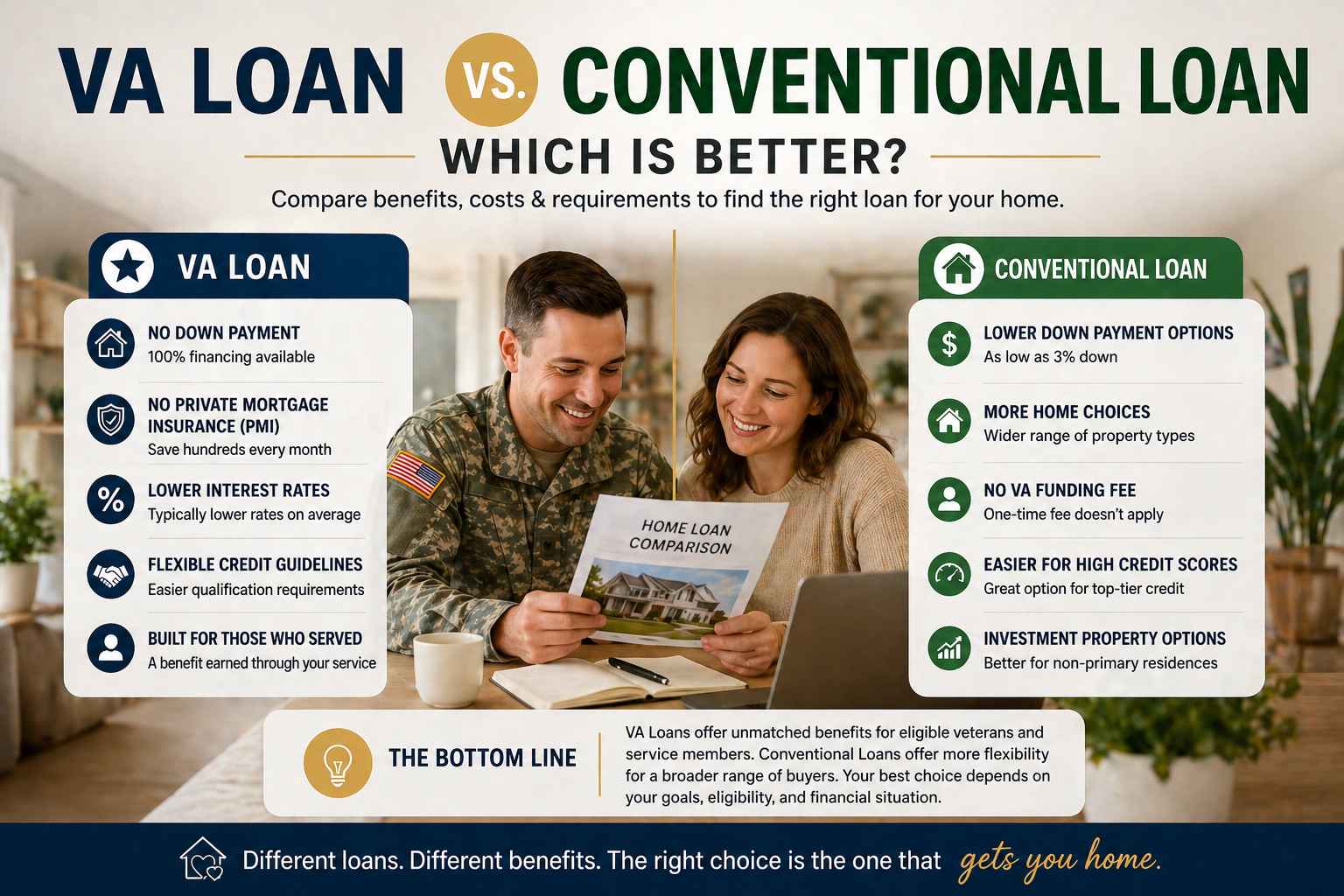

- VA loans Once an exclusive perk of eligible veterans, active-duty military and surviving spouses, VA loans generally require no down payment while also avoiding private mortgage insurance (PMI) entirely.

- Conventional loans, on the other hand, are open to everyone who qualifies and do not have military service requirements while typically requiring a down payment (and will mandate PMI if you put down less than 20%).

- VA loans generally have much lower interest rates than conventional loans because they are backed by the government, which lowers risk for lenders.

- VA loans are limited to primary residence use, which means that loan proceeds may only be used for the purchase of a home that will serve as your primary residence; while conventional loans have no such limitation and can be used for other types of real estate purchases including second homes or investment properties.

- VA loans charge a funding fee, although conventional loans tend to have lower upfront costs or ongoing PMI — making the best pick for you situation-dependent.

What is a VA Loan?

What is a VA loan? In a nutshell, it is a home loan that can be originated specifically for our country’s heroes – Veterans, Active-Duty service members, and eligible surviving spouses.

Those loans have the full faith of the U.S. Department of Veterans Affairs behind them, a big deal, to be sure. It means that a percentage of the loan is backed by the government, and therefore, lenders are more inclined to offer competitive terms.

I have always researched the advantages of VA loans and they really do excel. One of the primary benefits is that, if you qualify and have full entitlement, it allows for zero down payment on a home. Seriously, zero down. In contrast to many other types of loans, where a lot will need to be scraped together at the outset, this is a massive benefit.

There are costs associated with VA home loan benefits that are not limited to the down payment. This means you typically won’t have to pay mortgage insurance, which is designed to protect the lender in case you’re unable to make your mortgage payment.

And on top of that, VA loans typically come with some quite competitive interest rates (and often lower than you’ll probably find elsewhere). All: To make it easier for those who served to own a home.

Who Qualifies for a VA Loan?

So, who qualifies and gets to use this great VA loan program? That is rather specific, and that’s part of what makes it a great deal for those who qualify. In short, if you have served in the U.S. military, then you might be eligible. Among those are veterans, active duty service members and even some spouses who survived the military.

Obtain a Certificate of Eligibility In order to get the ball rolling, you need something called a certificate of eligibility or too put it simply a COE.

This simple document tells the lender that your loan is supported by the Department of Veterans Affairs (VA). Receiving your COE is usually a relatively simple process that can be done online through the VA’s portal or your lender can assist you. This is a vital step to make use of these military home purchase benefits.

On top of that, there are also a couple other things to be aware of beyond just service. You will be vetted by having lenders pull your credit, check your income and the property you want to purchase. Although the VA does not establish a minimum credit score, many lenders prefer to see a score of at least 620.

It will also ensure that you have computed income, represented in a way to cover monthly payments. Also, VA loans are for your primary residence, not a second home or an investment property.

Unlike many of the other assistance programs, VA loans are also meant to provide substantial financial incentives — such as no down payment and no private mortgage insurance costs, thus ensuring that homeownership is affordable for folks who have served our country. This is absolutely one of the best mortgage options for veterans.

So here is a rundown of the key VA loan eligibility requirements:

Referral: There is a requirement for a minimum service length. This will depend on your time of service but generally, you must have served 90 days of active-duty service during wartime; 181 days of active-duty service during peacetime; or 6 years in the National Guard or Reserves.

- Certificate of Eligibility (COE): Your golden ticket from the VA.

- Credit Score — The VA does not set a specific credit score; however, lenders generally prefer borrowers to have scores of 620 or higher.

- Income — you must convince the lender that you earn enough income to make the mortgage payments and any other debt payments (if any).

- Make sure the home at from your Primary Residence

Getting a grasp on who can utilize these VA mortgage perks is the first step to understanding how lofty these benefits are. It is about acknowledging the sacrifices and giving tangible ways to those who are privileged enough to own a home.

What is a Conventional Loan?

This begs the question: What is a conventional loan exactly? Simply, what it is, is a mortgage that has no support of any government entity like the VA or FHA. Instead, loans like these conform with government-sponsored enterprise guidelines established by Fannie Mae and Freddie Mac.

For anyone else who neither is eligible for or choose not to utilize a government-backed loan, they are basically the standard very nearly any homebuyer.

Consider them the obvious choice for many. Since they are not pegged to specific military service, all applications must meet the lender’s financial qualifications. This makes them so accessible to a huge cash of buyers.

So, give or take a few things that you need to know generally speaking:

Eligibility: Open to everyone, as long as they qualify with the lender’s credit and income requirements. No military service is required.

Down Payment: Although you may find options with a down payment of as little as 3%, you can typically avoid private mortgage insurance (PMI) by putting down 20% or more.

Mortgage Insurance: If you put down less than 20%, you’re probably going to have PMI. This is a safeguard for the lender—not you—and increases your monthly payment.

Property Types: Conventional loans are used for a variety of property types, ranging from primary residences to second homes, and even investment properties.

Conventional loans are a popular option for many homeowners since they do not come with the same eligibility requirements as those backed by the government and are relatively easy to secure. They are flexible with what they allow, so if you dont mind a down payment and PMI it can be a great option.

Since I had some savings to put down for a mortgage, traditional loans were great when I researched what would be available to me. I assumed the path to homebuyers was simple and I would not have to meet other service goals.

Unless you’re a veteran or an eligible surviving spouse, the conventional loan would most be your most viable option to purchase a home, and there are literally hundreds of lenders offering them. They are useful to experiment with different traditional loans and see your budget functional within it.

Who Qualifies for a Conventional Loan

So you are considering a conventional mortgage? I get it. They’re a really popular option for purchasing a home, and with good reason.

Unlike VA loans, which have specific service requirements, conventional loans are pretty much just open for business to anyone who meets the lender’s criteria. That means a whole lot more people can use them.

Types of Conventional Loans

Specifically, I mean the kind that is referred to as a “conforming” loan when I talk about conventional loans. These are the loans conforming to guidelines set by Fannie Mae and Freddie Mac, two of the largest purchasers of mortgage loans from lenders.

The fact that they are so standard can often make them cheaper. Then there are the “non-conforming” loans, which fall outside those guidelines (the loan amount is too high or some other peculiarity). These are a little more difficult to obtain and likely will come with higher rates.

In order to even step through the door with a conventional mortgage, you have to meet some basic requirements for a conventional mortgage. This usually involves:

A good credit score: Whatever lender you’ve looking to land a loan with probably will want to see a score around 620 or above. If your score is higher, like 740 or over, you may get better terms. I always look at my credit report before applying, just to see the score.

Proof of income and employment: Lenders want to see how well you are employed and can support that monthly payment. They will typically request pay holdem poker payday710 site prison title living dead online demo 7/soil use paper, tax returns and bank statements.

Control over the Debt-to-Income ratio: This is basically a comparison between how much you owe each month and your overall earning. Lenders typically want to see this ratio under a certain percentage, usually about 43%.

A down payment: Some loans allow a buyer to put 100 percent down, but conventional loans usually require an amount. The minimum is usually about 3%, but leaving 20% or more can help you skip private mortgage insurance (PMI) entirely.

Just keep in mind that traditional loans are fairly forgiving as to property types. They are frequently available for primary residences, second homes, or even investment properties which isn’t always true with other types of loans.

I remember when I was researching my first house, the lender was really probing into my finances. They wanted to see everything, bank statements, W-2s, the whole nine yards. It was a little weird, but you understand they wanted to confirm I could actually afford the place.

Isn’t that all just part of the run-of-the-mill conventional mortgage deal anyway? If you’re in search of a loan that’s accessible to the general public and not tied to military service, then conventional loans are certainly worth your attention. Discover How To Qualify For This Loan Program If You Are Interested

MAJOR DIFFERENCES: VA Loan vs. Conventional Loan

Once I started researching how to buy a place, I discovered that there are all kinds of different ways one can secure a mortgage. Two of the biggest ones that kept rearing their heads were VA loans and conventional loans. On the surface, they might sound alike — but once I started to dig in, I found some pretty stark differences between VA and conventional loans that are worth noting.

Down Payment Requirements

This is a big one for many people, including me. A VA loan typically offers 100% financing. This can mean that, in many circumstances, you do not even need a down payment. Pretty wild, right?.

Conversely, conventional loans typically require a minimum of 3% down, and when you put down less than 20%, you’ll likely be responsible for private mortgage insurance (PMI). This, in itself, makes the VA loan advantageous if you truly struggle at all to save a hefty portion of liquid assets for a down.

Interest Rates and Fees

This comparison of VA and conventional loans also naturally carries a review of the costs. VA loans are a government-backed product, which typically allows lenders to offer lower interest rates. It’s a perk of serving our country.

But VA loans also have a thing called the VA funding fee. A fee, which is a percentage of the loan amount, to help cover program costs for taxpayers. You can roll it into your loan, meaning you don’t exactly pay for it upfront but be warned, it’s an expense to factor in. That’s not a fee you’ll find with conventional loans, but as I said above you may have PMI on a monthly basis that increases your payment due.

Mortgage Insurance

It all circles back to the down payment. With a traditional mortgage and less than 20% down, you’ll be paying PMI. It’s essentially insurance for the lender in case you don’t pay. It is extra added to what you pay monthly for housing.

Unlike conventional loans, VA loan holders do not have to pay PMI at all — with one exception. This can potentially save them thousands of dollars over the life of the loan and make home ownership more affordable for those who qualify. This is one of the key differences between VA and conventional mortgages that can really affect your ability to budget.

Different types of loans also have variations when it comes to the property type. VA loans can only be used on the house you also call home. Conventional loans are much more flexible; you may make use of it to get a vacation house or spend money on rental properties.

I found that knowing these differences helped guide me to see which path might have been more suitable for my circumstances as I explored my options. Their performance isn’t all about the numbers, either: It’s about what works for your life and where you want to go.

So when I need to purchase a rental property, a conventional mortgage is my alternative. But for my main home, VA loan benefits were a real draw. At some point, you know the need of interests here for your home loans.

Interest Rates – VA Loan vs Conventional

While I was researching on purchasing my place, the interest amounts on the loans were a big point. Every lender seemed to have a different number and we just didn’t know what was good. VA loans seemed to be slightly lower than the conventional loan rates that I had been reading.

That seems logical, given that the government backs them and apparently lenders feel much safer buying mortgages when they are backed by these agencies. I also came across some data showing that VA loan rates were approximately 0.25% to 0.50% lower than conventional ones It may not seem like much, but year after year it really mounts up.

A little difference in the interest rate can be a matter of hundreds to thousands, if not tens of thousands, at the end of that loan. And not just the rate itself, however. And you have to consider the entire picture.

Some VA loans carry a funding fee, which is simply a one-time payment. Most of the time, there is such a thing with conventional loans but it can come along with private mortgage insurance if you don’t put a good amount of cash down. So, yes, I learnt that although the interest rate advertised is great, it is just one part of the whole equation.

Let’s take a peek at how they usually measure up:

VA Loans: They usually have a lower advertised marketed rate because of the fact that, they are guaranteed by the VA. This can result in major savings over the duration of the loan. There is no down payment; however, there is a VA funding fee, depending on your service and when/how much you put down.

Conventional Loans: Some of the most competitive rates out there, particularly if your credit score is high and you can make a larger down payment. If you make a down payment of less than 20%, you’re likely required to pay private mortgage insurance (PMI), which increases your monthly outgo.

The key here is to compare the overall cost not just the top level interest rate. I realised that an APR (Annual Percentage Rate) View, with the fees factored in gave me a more real sense of a comparison, To me, a well below market rate VA loan with a funding fee was the less worse choice since I wasn’t sitting on much of a down payment. A lender will be able to speak with you about your specific situation, what makes the most sense for your financial goals.

Which Loan is Right for You?

Fine, so you have been researching your choices on purchasing a domestic and also you are attempting to determine what home loan is higher, the VA mortgage or maybe a standard loan. This really depends on your individual circumstances and budget. This is where understanding mortgage products comes in.

For many veterans and service members, the VA loan is a no-brainer. Just think about this: if you have full entitlement, ZERO down payment required. That is one big obstacle that has been removed right off the bat. And you donât even have to pay private mortgage insurance, which can be quite the chunk of change over time.

Veterans’ Affairs Interest rates: VA interest rates have also been fairly competitive, often lower than conventional loans. This is a benefit for service and, when used correctly, can lead to homeownership as a possible reality.

But in some cases, a traditional loan could be just the ticket. With a conventional loan, if you’ve managed to save at least 20% for your down payment, then private mortgage insurance won’t be an issue either. This can be a big deal. And of course, conventional loans have a little more leeway if you’re planning to buy the place as your second home or an investment property; VA loans require you to live in the home you’re financing.

Here are some of the main differences at a glance:

Setting an amount down: Alaska loan principles regularly require no first installment while traditional advances expect somewhere in the range of 3-5% to be put down just to begin, and 20% is needed to keep away from Private Contract Protection (PMI).

Unlike PMI with other loan programs, VA loans do not require mortgage insurance. PMI is required for conventional loans when the borrower puts down less than 20%.

Property Use: VA home loans can only be taken to purchase a primary residence. Conventional Loans: These loans can be used for primary residences, second homes and investment properties.

Who is VA loan for: VA loans are for eligible borrowers who are servicemen, veterans or Surviving spouses. Conventional loans are accessible to anyone with sufficient credit history and income.

At the end of the day, the ‘better’ loan is one which suits your financial situation and your homeownership ambitions. For many, with access to a VA mortgage option, nothing comes close to the upfront savings and ongoing benefits you would receive.

However, if you cant get a VA loan and dont have specific investment goals, then a conventional mortgage is the best option. Talk to a lender who has both types of loans available and see which one makes the most sense for you. For more information about VA loan benefits, check out the Department of Veterans Affairs website.

When considering buying my first house, I capitalized on all the things a VA loan afforded me because saving for a down payment seemed unbeneficial at that time. It lifted a great deal of worry off our shoulders not to have to pay PMI.

It just made everything feel less overwhelming. However, I know people who had a decent down payment saved up (enough to avoid PMI) and instead of going with an FHA loan chose the flexibility of conventional financing later down the line. So much depends on what you want now and need later.

So, Which Loan Should I Go For?

When breaking all this down, I could totally understand why the decision between a VA loan and a conventional loan is not so cut-and-dry. The VA Loan seems like a no-brainer if I can qualify to live in the house myself. Dramatic savings in the short and long term by avoiding a big down payment and foregoing private mortgage insurance.

However, if I were going to purchase a rental property or second home, or if I simply had a sizable down payment cash in reserve, I would just get a conventional loan. It truly just depends on what you plan to use the house for and how your finances are looking at this very moment. There is no one-size-fits-all answer to the question, but understanding the differences, this makes the decision a lot easier.

Frequently Asked Questions

What is the biggest advantage of a VA loan over a conventional loan?

The biggest turn-on for a VA loan is not having to come up with a down payment and no private mortgage insurance payments. This saves my a ton of money up front and every month.

Who gets to use a VA loan?

VA loans are for veterans, active duty military, and some surviving family members. You have to prove your military experience, by having a Certificate of Eligibility.

What about VA loans — do I have to pay private mortgage insurance with them?

Nope! That’s one of the best parts. Another monetary incentive of VA loans is that I will not have to pay private mortgage insurance (PMI), which is a big cost saver for me over the life of the loan.

Can I obtain a VA mortgage to purchase an investment property?

Sadly, no. VA loans can only be used for purchasing a place I intend to live in. For example, if I wanted to purchase a vacation property or a strictly rental unit, I would have to investigate conventional financing instead.

Why do VA loans get special attention when it comes to credit scores versus conventional loans, you ask?

Overall, VA loans are usually more lenient. I can qualify for a credit score of 580. FHA loansWhereas traditional loans typically look for a score 620 or above.

Is it harder to get approved for a VA loan over a conventional loan?

They are not necessarily harder, but they have rules related to military service. Furthermore, the VA sets conditions for the state of your home, which means I don’t get that option to waive an appraisal as some traditional buyers can do in a hot market. They can, however, also be easier to qualify for financially.